New paper: Testing machine learning systems in real estate

How do ML-models arrive at their predictions? Do they do what we hope they do—or are corners cut?. New paper out at Real Estate Economics

How do ML-models arrive at their predictions? Do they do what we hope they do—or are corners cut?. New paper out at Real Estate Economics

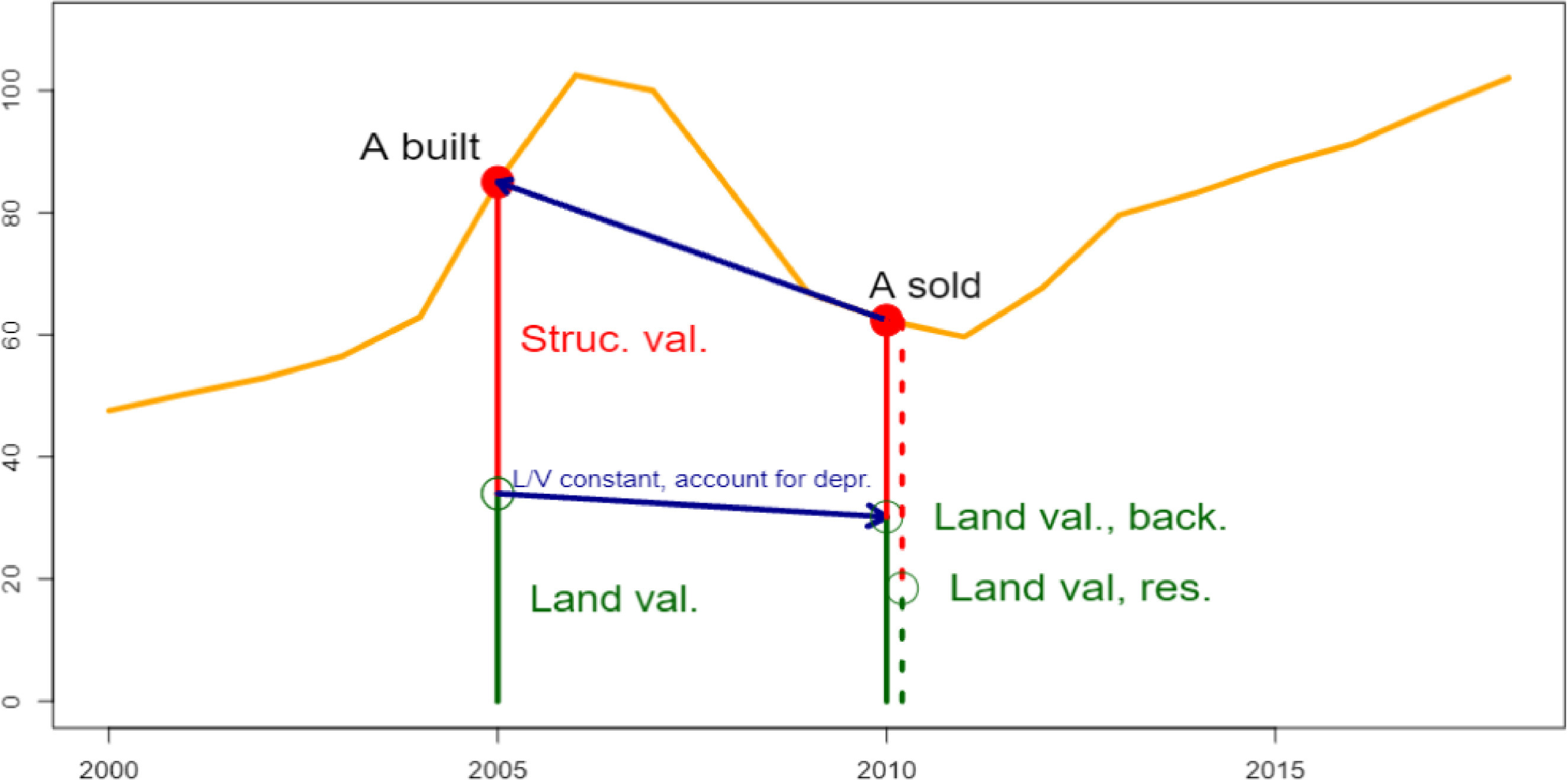

Paper out: This paper develops a new approach to estimate the value of urban land and indirectly tests land residual assumptions. Bonus: Value surfaces estim...

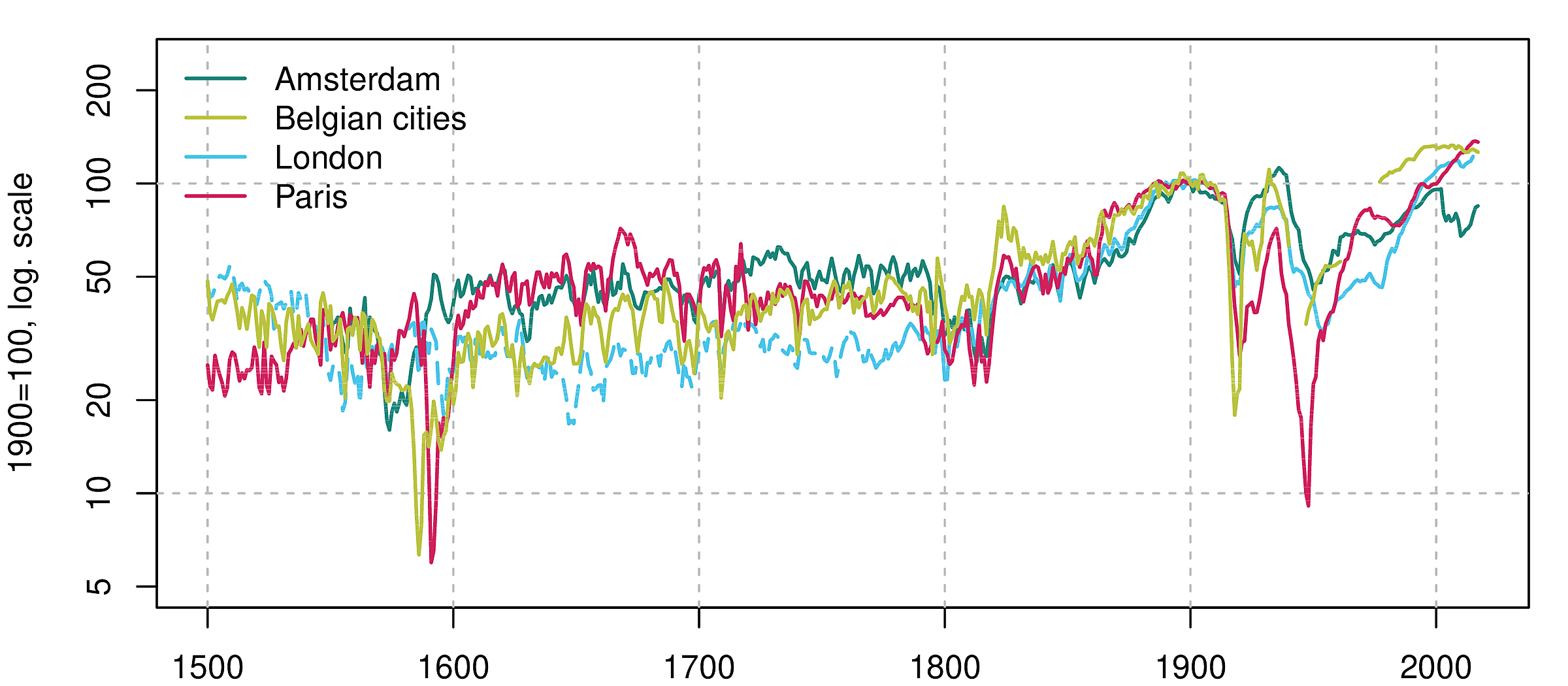

This paper studies urban rental prices for half a millennium (1500–2020) and seven cities: Amsterdam, Antwerp, Bruges, Brussels, Ghent, London, and Paris. Ba...

A neural networks that accounts for spatial correlation and time dynamics?

New paper out: A closer look at urban land and structure values – this is important for national accounts and for analysis of real estate risk over time. Wit...

Summary of our total return paper in German and French.

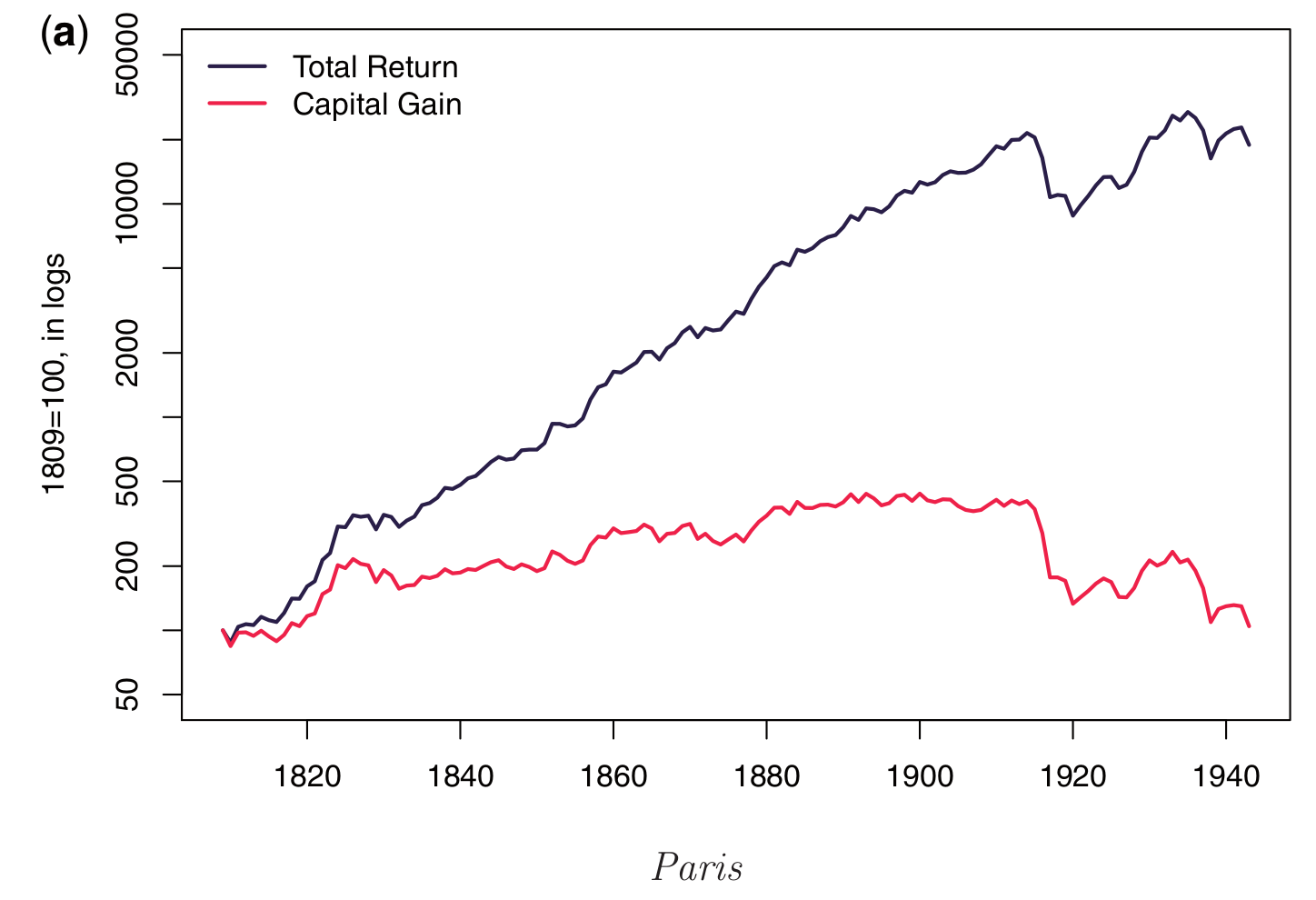

New research accepted for publication at the Review of Financial Studies (RFS) suggests that returns to real estate are solid but not exceptional: No sign of...

New research accepted for publication at the Journal of Real Estate Finance and Economics: This paper couples a traditional hedonic model with architectural ...

This paper first collects binary classifications of house pictures from a large group of participants and then trains personalized ML classifiers for each pa...

This article estimates the first constant quality price index for Internet domain names. The suggested index provides a benchmark for domain name traders and...

New paper out: A closer look at urban land and structure values – this is important for national accounts and for analysis of real estate risk over time. Wit...

Summary of our total return paper in German and French.

New research accepted for publication at the Review of Financial Studies (RFS) suggests that returns to real estate are solid but not exceptional: No sign of...

New research accepted for publication at the Journal of Real Estate Finance and Economics: This paper couples a traditional hedonic model with architectural ...

This paper studies urban rental prices for half a millennium (1500–2020) and seven cities: Amsterdam, Antwerp, Bruges, Brussels, Ghent, London, and Paris. Ba...

This paper first collects binary classifications of house pictures from a large group of participants and then trains personalized ML classifiers for each pa...

Paper out: This paper develops a new approach to estimate the value of urban land and indirectly tests land residual assumptions. Bonus: Value surfaces estim...

A neural networks that accounts for spatial correlation and time dynamics?

This article estimates the first constant quality price index for Internet domain names. The suggested index provides a benchmark for domain name traders and...

How do ML-models arrive at their predictions? Do they do what we hope they do—or are corners cut?. New paper out at Real Estate Economics

Etchings by Franz Xaver Rektorzik, printed by August Potuczek